The human catalyst

A strong Human Capital Factor ignites growth.

“I only want to invest in fundamentals.” Such is a common statement from financiers. Yet these self-proclaimed ‘fundamental investors’ are people who regularly ignore a key aspect of a successful business.

The term ‘fundamental’ is used to describe financiers who back companies only when the hard financial data available to them looks positive. While the approach might sound sensible, it is limited – because the available data is insufficient and inadequate.

One of the fundamental predictors of growth that goes largely unquantified is human capital – the people power within a firm that drives it forward. Human capital is a sort of free energy for businesses. When harnessed, it acts like a perpetual motion machine, igniting growth by making companies more innovative, creative, productive, efficient and agile. But, because analysts have struggled to measure it, it is challenging to consider as an input for investment decisions. Irrational Capital is trying to change that with a new metric: the Human Capital Factor™(HCF).

The Human Capital Factor

Irrational Capital mines a plethora of disperse data to create the HCF. Sources include company survey data and publicly available assessments, including reviews on recruitment sites, such as Glassdoor. Some sources are relatively nascent. For example, Glassdoor is a household name now, but only came into existence in 2007. Yet it has been possible to back-test the performance of companies with a high-HCF versus the market benchmark. The results are illuminating.

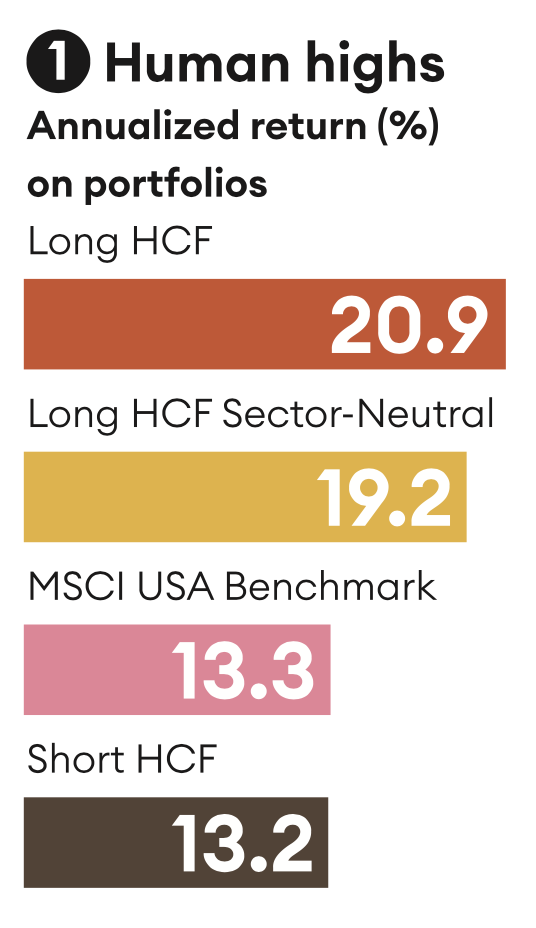

To analyze the HCF, JP Morgan used the MSCI USA Index, which comprises more than 600 stocks. It formed and tested two share portfolios for the years between 2009 and 2020. As of 31 December in each year, it placed a concentrated portfolio of 30 stocks with the highest HCF scores in the long-HCF portfolio. The 30 stocks with the lowest HCF scores were assigned to the short-HCF portfolio. The portfolios were weighted and regularly rebalanced, to ensure a fair comparison.

The results tell a clear story. The high-HCF portfolio achieved an annualized return of +20.9%, compared to just +13.3% for the MSCI overall. When the high-HCF portfolio was rebalanced to make it ‘sector-neutral’ – reflecting the sectoral composition of the MSCI benchmark – the difference remained profound. The sector-neutral high-HCF portfolio showed an annualized return of +19.2%, substantially higher than the Index benchmark (see Figure 1).

Heavy hitters

One fascinating element of HCF is the way it cuts across all branches of the economy. When we set about quantifying HCF, we’d expected it to be a major factor in the so-called knowledge economy – capital-light firms such as Google and Meta. We had anticipated it to be a less important factor in sectors like manufacturing. The surprise was that HCF is as vital for capital-heavy industries as for capital-light sectors. Why is this? One example might shed some light.

I met Joe, an engineer who worked at a pipe company. The company is unable to use oil as a lubricant when manufacturing its pipes, so it uses molten glass. The raw glass was sourced from recycled car windshields from a major car maker.

The pipe-maker had a problem: a greater proportion than expected of its pipes were cracking and failing, and nobody knew why. Out of an interest in and devotion to his job – not because he had been asked – Joe took it upon himself to do some detective work.

After about two years of self-driven investigation, Joe solved the problem. Car companies were incorporating metal into their windshield glass so the windshields could double-up as integrated radio antennae. The ratio of metal to glass was tiny, but sufficient to make the pipes inordinately prone to cracking. Mystery solved.

One man’s personal mission to solve a critical problem led to huge productivity gains for his company. Its high HCF was evident.

The happiness paradox

Many would assume that the pipe-maker detective, Joe, was self-motivated because he was ‘happy’ in his job. Yet the idea of happiness is over-egged and frequently misused in business. Most humans derive happiness from leisure, not work. Many of us would be truly happy in the moment we found ourselves sitting on a tropical beach, cooled by a pleasant breeze, sipping on a well-mixed mojito. Happy, but unproductive.

Rather, a high HCF comes from a combination of task satisfaction, feeling appreciated, psychological safety, and the degree to which companies provide the conditions where employees can align their own utility with that of the company and its stakeholders. This combination is more related to meaning than happiness. Task satisfaction is the reward one gets from completing a challenge: say, running a marathon, rather than an undemanding leisure activity, such as drinking a cocktail. Psychological safety, meanwhile, is usually derived from a healthy company culture. It gives employees the confidence to challenge decisions, the agency to influence the direction of their company.

Joe expended excess time and energy on an investigation because he wanted to do it. He had intrinsic motivation – and he enjoyed the psychological safety of knowing that he would be listened to when he challenged the use of materials from a longstanding supplier.

Psychological safety is also an antidote to groupthink, a strong predictor of inertia and restricted growth. Rather than being a function of momentary happiness, it gives employees the internal strength to express their real feelings and ideas, and even their dissatisfaction with some aspects of

the company.

When Joe investigated the supply chain and found the weak point, it was not easy news to share, but, because of a high HCF at his company, he felt empowered to do something about it. His company appreciated his efforts and, by changing a policy based on his evidence, benefited commercially from them.

The motivation formula

Intrinsic motivation is like a perpetual motion machine for companies, an invisible, free fuel for growth that can be nurtured in all workers, provided the conditions are right.

Remember the last time you visited a large, branded store and the sales assistant went out of his way to help you? He might have checked the stockroom when the product you wanted was absent from the shelves. He might have called other local branches to check whether it was in stock nearby. That experience is likely to have added to your loyalty with that chain; it added indirect value to the company by making it less likely that you will choose its competitors in future. It also potentially added direct value – by making it more likely that the chain would make another sale. When we think about it, it is easy to visualize equivalent examples, where employees across the board have added value through their own acts, in every sector of the economy.

So, what drives intrinsic motivation? When we explored the factors that contribute, some key findings emerged. It transpires that absolute benefits tend to have only a marginal effect at best: for example, the level of one’s salary is a lesser factor than fairness in the salary structure; the scale of one’s retirement benefits is also a lesser factor than the degree to which those benefits are seen to be distributed equitably. Other factors, such as low levels of bureaucracy and a general feeling of being appreciated by one’s colleagues, are better predictors of intrinsic motivation than financial rewards. Together they drive a key pillar of high HCF – goodwill.

Goodwill is the range between the minimum effort required by an employee to keep her job and the maximum effort possible by that employee if she is fully engaged in her role. The most illustrative study on the factors behind goodwill (Bareket-Bojmel, Hochman and Ariely, 2017) reveals that non-monetary appreciation, such as verbal or written praise, led to productivity increases in the study group – microchip production workers. By contrast, gold did not glitter: monetary bonuses led to a long-term decline in productivity.

The fundamentals of HCF

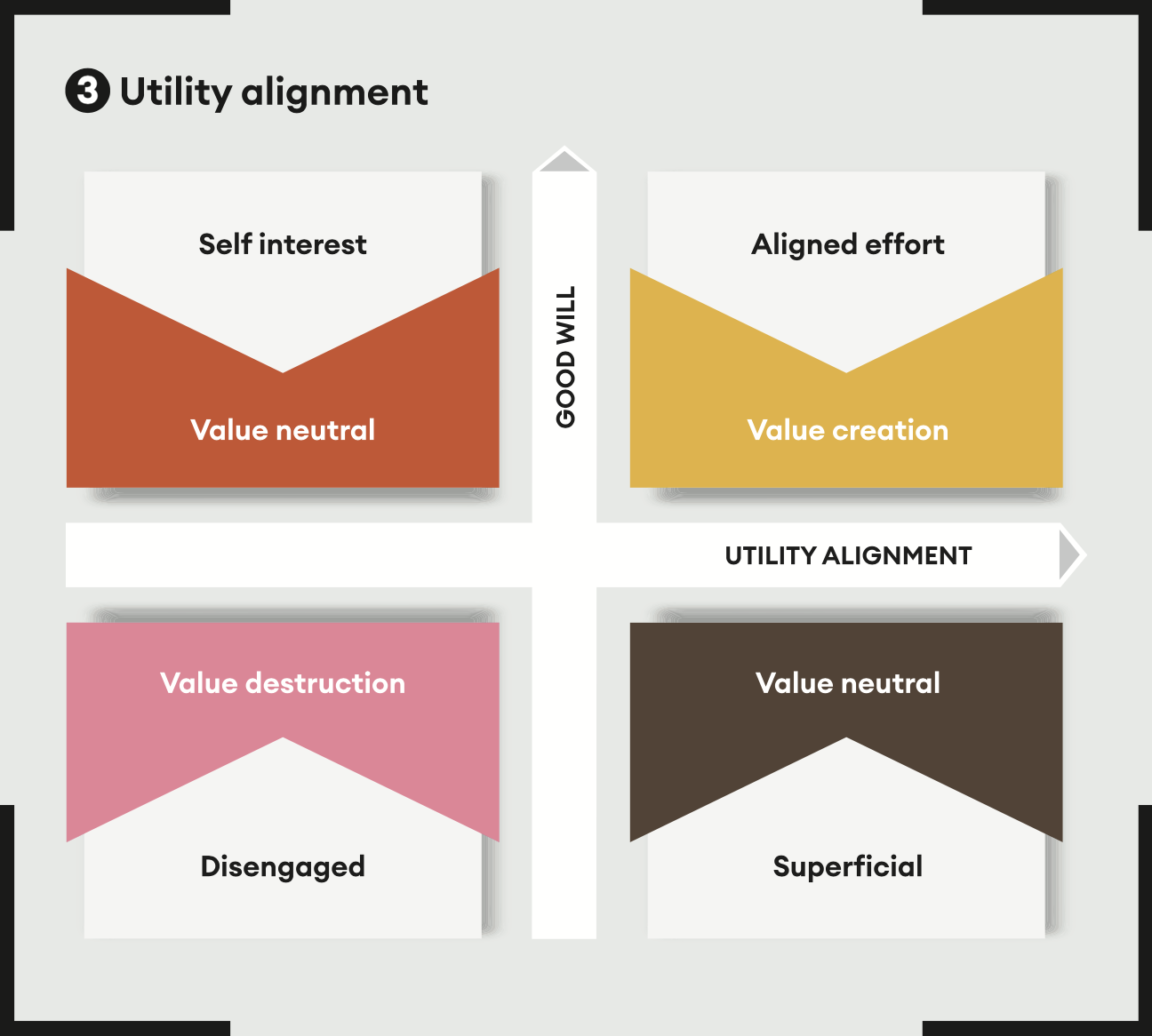

Goodwill is imperative for a high HCF, yet it is just one of two key building blocks. The other is utility alignment – the willingness of employees to execute tasks that are aimed at the wider benefit of the company. An employee with high levels of goodwill will not achieve her full potential if she is unaligned with the goals of the company (see Figure 3).

Let us return to our branded store by way of an example. Imagine the chain employs several beauticians to sell its makeup. The beauticians offer free makeup consultations for customers. Their hope is that at the end of each makeover, they will sell the makeup they used.

One day, a beautician notices that the customer could benefit from a face cream that is manufactured by the company, but is unavailable at the makeup counter. It is stocked elsewhere in the store, in the skincare department.

The beautician asks the customer to wait and visits another corner of the store to bring the product in question to the customer. Because the product is stocked by a different department, the beautician gains no commission from the sale. Indeed, if the customer buys the other product they likely spend less on makeup. While the beautician makes no financial gain from the sale, it is nevertheless beneficial for the company and its customer. The beautician recognizes this and acts accordingly. This is what utility alignment is all about.

As Figure 3 shows, when either goodwill or utility alignment are lacking, value is neutral. Where both are lacking, value is destroyed. Yet, when both goodwill and utility alignment are present simultaneously, a lot of value is created. The workforces of companies with high HCF are clustered in this quadrant.

The future bottom line

Traditional accounting considers human capital an ‘intangible’ – something that cannot be measured. Yet Irrational Capital is putting a dent in this traditional practice. Not only can it be measured, it can also be invested in. Through Harbor Capital we offer three exchange traded funds that comprise high-HCF stocks: HAPI, HAPY and HAPS.

The main point is that human capital is not an ethereal factor. It is real and calculable. As we have shown, it is possible to quantify HCF and demonstrate its effect on company performance and value over time. The data that informs the quantification – both public and private – has only become available in the last few years; it is continually being expanded and should become rapidly richer and more extensive.

As it relates to measuring and reporting human capital, traditional accounting is

somewhat limited. The Human Capital Factor is the opposite of intangible. It is demonstrating the ability to make a former intangible tangible; something you can reach out and touch – and invest upon. One day, companies might start reporting on their human capital in their financial statements – and so-called fundamental investors might at last recognize the true fundamentals of business success.

Originally posted on December 1st 2023 here https://dialoguereview.com/the-human-catalyst/

Tweet

Tweet  Like

Like